India Pharma Outlook Team | Monday, 29 June 2026

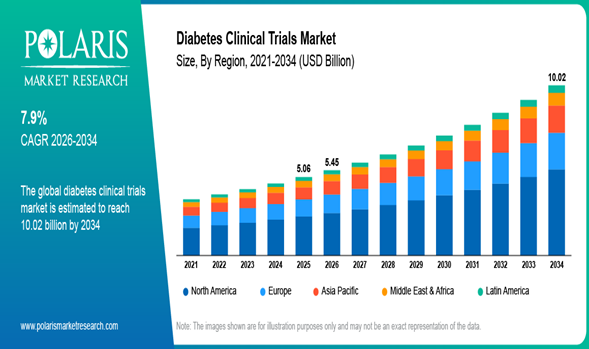

The global diabetes clinical trials market is on a steady upward trajectory, projected to grow from USD 5.45 billion in 2026 to USD 10.02 billion by 2034, at a CAGR of 7.9 percent, according to a comprehensive new industry analysis.

The diabetes research landscape is undergoing one of its most active periods in decades. Rising global diabetes prevalence, an explosion of GLP-1 receptor agonist research, and the rapid adoption of AI-enabled decentralized trial models are converging to push pharmaceutical and biotech pipelines into overdrive.

According to the latest Diabetes Clinical Trials Market research report by Polaris Market Research, the market was valued at USD 5.06 billion in 2025 and is set to nearly double over the next decade as sponsors race to commercialize next-generation metabolic therapeutics.

The scale of the underlying disease is staggering. The International Diabetes Federation estimates that roughly 589 million adults aged 20–79 were living with diabetes worldwide in 2024 — a number expected to swell to about 853 million by 2050. That expanding patient pool is translating directly into trial volume, recruitment demand, and R&D investment across Type 1, Type 2, and obesity-linked diabetes indications.

In the United States alone, the CDC's National Diabetes Statistics Report puts the diabetic population above 40 million, including more than 2 million Type 1 patients — a concentration of disease burden that helps explain why North America commands the largest regional footprint in this space.

Also Read: Scaling Perfusion Technology from Lab Success to Manufacturing Reality

If there's one therapeutic class defining this market cycle, it's GLP-1 receptor agonists. These drugs captured 29 percent of therapy-type trial share in 2025, fueled by their dual role in glycemic control and obesity management. The commercial success of semaglutide and tirzepatide has triggered a wave of follow-on research into combination therapies, cardiometabolic outcome studies, and next-generation incretin-based treatments.

That momentum isn't slowing down. In February 2026, Eli Lilly reported that its oral GLP-1 candidate orforglipron outperformed oral semaglutide on blood sugar control and weight loss in a head-to-head Phase III trial — a result likely to intensify competitive R&D spending across the sector. Meanwhile, SGLT2 inhibitors, prized for their kidney-protective and cardiovascular benefits, are emerging as the fastest-growing therapy segment, with a projected CAGR of 8.2 percent through 2034 as sponsors increasingly test SGLT2–GLP-1 combination regimens.

By trial phase, Phase III studies led the market with 43 percent share in 2025, reflecting the sheer scale of late-stage commercialization activity for insulin analogs, GLP-1 agonists, and cardiovascular outcome therapies. Phase II trials, however, are the fastest-growing segment at a 7.2 percent CAGR, propelled by innovation in stem-cell therapy and beta-cell replacement research targeting autoimmune diabetes.

Study design tells a similar story of transition. Interventional studies still dominate with 64 percent share, but decentralized clinical trials are growing fastest of all, at a 10.5 percent CAGR — the single highest growth rate of any segment in the entire report. Wearable glucose monitors, telemedicine integration, and AI-enabled remote patient monitoring are making it possible to run diabetes trials with far less site dependency than before. A notable proof point: in February 2025, the University of Virginia ran a clinical trial on an AI-enabled diabetes treatment tool designed to automate insulin delivery and glucose monitoring for Type 1 patients — exactly the kind of decentralized, tech-forward study sponsors are now scaling.

For a full country-by-country breakdown, including segment-level forecasts across all major markets, the complete regional analysis in the diabetes clinical trials market report offers granular data through 2034.

Pharmaceutical and biotechnology companies remain the dominant end users, commanding 49 percent market share in 2025 on the back of robust late-stage diabetes programs and biologics development. Contract Research Organizations (CROs) are the fastest-growing end-user segment, expanding at an 8.0 percent CAGR as sponsors increasingly outsource site management, patient recruitment, and decentralized trial operations to manage rising complexity and cost.

Key players shaping the competitive landscape include AbbVie, AstraZeneca, Biocon, Boehringer Ingelheim, Eli Lilly, GlaxoSmithKline, Johnson & Johnson, Merck, Novo Nordisk, Novartis, Pfizer, Sanofi, Servier, Takeda, and Wockhardt — a roster spanning Big Pharma incumbents and specialized biotech innovators alike.

Regulatory tailwinds are also reinforcing commercial momentum: in April 2026, the U.S. FDA approved the first generic dapagliflozin tablets for Type 2 diabetes with cardiovascular benefits, widening patient access to SGLT2 inhibitor therapy and reinforcing the broader diabetes therapeutics ecosystem that clinical trial activity feeds into.

High operational costs remain the market's primary headwind. Long observation periods, complex compliance requirements, and the difficulty of recruiting and retaining patients for cardiovascular outcome and late-stage diabetes studies all add up. Rising data management costs compound the challenge further.

The clearest counterbalance is AI-driven decentralization. By cutting enrollment timelines, enabling remote monitoring through wearables and continuous glucose monitors, and powering predictive patient-identification algorithms, AI-enabled trial models are giving sponsors a real lever to control costs while improving retention — a trend the report identifies as the single biggest opportunity area through 2034.

With obesity and diabetes therapeutics converging, GLP-1 and SGLT2 pipelines expanding, and decentralized trial infrastructure scaling fast, the diabetes clinical trials market is entering a phase of structural, technology-driven growth rather than simple demand-led expansion. Stakeholders — from Big Pharma sponsors to CROs and digital health vendors — that move early on AI-enabled, decentralized trial models are best positioned to capture share as the market more than doubles by 2034.

.jpg)