Samrat Pradhan, Managing Editor at India Pharma Outlook

Pharma CDMOs (Contract Development and Manufacturing Organizations) in India brought forth a strategic shift in the ever-important drug development process for pharma companies.

Today, Indian CDMOs are evolving beyond the traditional model to stay relevant in today’s volatile market with the CDMO 2.0 model. These players today are not just mere contract developers and manufacturers, but rather have evolved into more strategic, tech-agnostic partners offering a one-stop solution.

If we speak of the term Pharma CDMO 2.0, it represents a dramatic shift from transactional manufacturing to integrated solutions deliverability with rapid scale capabilities for the ever-evolving complex therapies such as biologics; thereby shaping the future of the pharmaceutical sector for good.

India is emerging as a preferred CDMO destination, thanks to its strong chemistry capabilities, lower production costs, and skilled workforce. According to McKinsey & Company, India’s CDMO market is expected to reach USD 20 billion by 2030, with a focus on formulation development, API manufacturing, and biologics.

Indian CDMOs are also investing in USFDA-approved plants, tapping into regulated markets and forming long-term partnerships with leading pharma companies in the US, Europe, and Southeast Asia.

According to InsightAce Analytic, Global Pharmaceutical CDMO 2.0 Market Size is predicted to grow at a 8.4 percent CAGR by 2034. The majority chunk of this growth will be aimed by Indian CDMOs.

North America is leading with a 35 percent share of the CDMO market, followed by Europe and the Asia Pacific region at about 28 percent each.

India’s market is witnessing a more significant growth and is predicted to outpace the global average with a CAGR of 14 to 15 percent to reach USD 18-19 billion by 2030.

However, to stay relevant in today's evolving CDMO landscape, players must make the required strategic shift, develop specialized capabilities, build robust regulatory strength, focs on talent development, and always be future-ready.

Today, pharma majors need CDMO partners who aren’t just service providers, but strategic collaborators. As outsourcing grows from being a cost-saving tactic to a core business enabler, the bar for selection continues to rise.

It is astounding to see how India is quietly building global-scale healthcare capabilities, wherein, indigenous CDMOs are playing a critical role in proliferating the space at global front.

These specialized service providers have become indispensable partners to both global pharma giants and nimble biotech firms, enabling faster innovation, cost-efficiency, and scalability.

As drug pipelines grow more complex and regulatory landscapes evolve, the rise of CDMO in the pharma industry is reshaping how medicines are developed and delivered.

Furthermore, speed and flexibility have become the cornerstone in the value driven CDMO 2.0 model. The growing complexity of drug development and the rise of biologics and call and gene (CGT), have given rise to DMOs who have carved a niche with its specialized manufacturing expertise.

On the other hand, it is important that CDMOs take proactive measures especially in today’s time surrounded by geo-political tensions, regulatory shifts and rising costs.

Today, pharma companies are shifting their development and manufacturing process to CDMOs due to several strategic and operational factors, be it in terms of cost-effectiveness, risk mitigation, speed to market, regulatory compliance, and innovation among other parameters.

Be it in terms of optimizing production, accelerating drug development process, or keeping robust quality control in place, advanced technologies such as AI & ML have been driving the much needed innovation in drug development and manufacturing.

AI capabilities have been aiding CDMOs in carrying out predictive maintenance and quality control measures by monitoring equipment in real-time, predicting failures before they occur, thus reducing downtime.

Furthermore, CDMOs are integrating continuous manufacturing capabilities rather than relying on traditional batch methods; thereby facilitating lower cost input, better efficiency, unhinged production, and most importantly faster time-to-market.

Process optimization via digital twins has helped CDMOs to devise electronic models of production processes to simulate thousands of conditions, allowing optimization without carrying out risky real production. It further helps in mitigating trail-to-error costs and facilitate scalability.

As a result, technology-enabled CDMOs are essential to the flexibility and responsiveness needed in the rapidly changing pharmaceutical industry, today. Just so to say, the technology has been elevated from enabler to engine.

Pinnacle Life Science reports that AI automates visual inspections, using machine learning to detect defects in drugs or packaging, ensuring high-quality output.

Neuland Labs notes that AI is used in Continuous Flow Reactor technology to improve process precision and reduce resource consumption.

Digital technologies like Enzene Biosciences points out, such as Electronic Batch Records (EBR), automate compliance with strict regulatory standards

CDMO 2.0 Model is bringing forth a paradigm shift in contract manufacturing, ushering in the new era of smart, integrated pharmaceuticals.

As we move forward with CDMO 2.0, it is wise to say that CDMOs must make the required strategic shift; evolving more than just contract manufacturing but also bringing to the table more comprehensive and robust models.

CDMOs often launch isolated improvement programs that fail to sustain impact. To thrive in the CDMO 2.0 era, transformation must become a permanent enterprise capability.

This requires a formal operations excellence engine, anchored by a central transformation office, clear accountability, and a rigorous performance cadence.

These teams must focus on continuous improvement, enable cross-site learning, and embed change capabilities across the organization. Structured effectively, this system fosters a culture of relentless improvement and creates a long-term competitive advantage.

We are witnessing a rise of Niche/ Modality-Specific CDMOs, wherein, CDMOs are specializing in specific modalities—such as lentiviral or AAV vectors, mRNA, or induced pluripotent stem cells (iPSCs) instead of "one-size-fits-all." For instance, players like Forge Biologics (gene medicines) and OmniaBio (cell therapy) are emerging as highly specialized, agile partners.

Adding to this, CDMO 2.0 model focuses on end-to-end one-stop-shop services deliverability to reduce handoff risks, leading CDMOs (e.g., Lonza, Catalent, WuXi Advanced Therapies) are offering integrated services—from pre-clinical plasmid DNA production to commercial-scale manufacturing and regulatory support.

As stated earlier, CDMO 2.0 is heavily invested in digital transformation which include driving automation to minimize human error, single-use bioreactor systems to prevent cross-contamination, and AI-driven predictive analytics for quality control.

Relationships are shifting toward strategic partnerships as CGTs require high capital investment. With this, CDMOs are collaborating with biopharma to co-develop processes, sometimes even providing early-stage capital or dedicated, exclusive suites (e.g., AGC Biologics).

The CDMO 2.0 model represents a shift from traditional, capacity-oriented service provision to a strategic, integrated partnership model that offers end-to-end solutions across the entire drug development and manufacturing value chain. This model integrates services like formulation development, API manufacturing, and clinical trial material services to accelerate timelines and reduce costs.

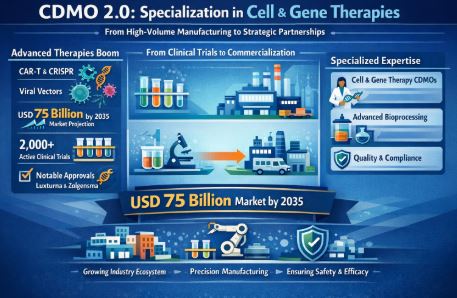

The specialization in biologics, cell and gene therapies (CGT) is a defining trend of CDMO 2.0, marking a shift from traditional, high-volume pharmaceutical manufacturing to a strategic, technology-driven partnership model.

As complex therapies—such as CAR-T cells, gene editing (CRISPR), and viral vectors—move from clinical trials to commercialization, they require specialized infrastructure and expertise that few biotech companies possess internally.

This trend is gradually reshaping the industry into a robust ecosystem rather than a purely transactional one.

The cell and gene therapy CDMO market is experiencing exponential growth, due to the surging demand for advanced modalities with projections to reach approximately USD 75 billion by 2035. This is driven by high-profile therapy approvals (e.g., Luxturna, Zolgensma) and over 2,000 active clinical trials.

In biologics, the method of manufacturing fundamentally defines the final therapeutic's safety and efficacy. Specialized CDMOs who have developed a robust 2.0 model are necessary to ensure consistency and compliance in sensitive biological materials today.

However, if we look at China’s push, the recent developments show that companies in China have obtained over half of multiple project agreements with US-based biotech firms, underscoring the competitive challenges Indian firms experience in this profitable sector. Hence, India must bounce back by inculcating higher-level research skills, sophisticated manufacturing setups, and expert personnel.

V Subramaniam, President at Reliance Life Sciences, said: “In the last seven years, China has come from behind and forged way ahead of India in biopharmaceuticals, driven by mission-driven govt policy, fast-track regulatory approvals and clearance of a huge drug approval backlog.”

“Recent project flows suggest Chinese companies have been able to secure more than half of their new orders from US-biotech companies, indicating Chinese companies’ operational scale, cost competitiveness and established capabilities remain unmatched,’’ said Tausif Shaikh, India analyst pharma and healthcare at BNP Paribas.

Shreehas Tambe, CEO & MD at Biocon stated, “India’s biosimilars industry is at a pivotal stage — the early years were defined by cost efficiency and established India as a reliable producer of high-quality generic medicines at scale. The next phase will evolve from cost leadership to capability leadership.’

“Though India has the broad capability, it has to address gaps such as cell line engineering depth, legal/IP plus market access firepower in the US, manufacturing at commercial scale of newer modalities from hybrid science like cell and gene therapies,’’ said Suresh Subramanian, National Life Sciences Leader, EY-Parthenon India.

According to market research firm, IQVIA estimates 118 biologics are losing patent protection in the US (2025–2034), representing a USD 232B global biosimilar market. India’s biosimilar exports, currently around USD 0.8 billion, are projected to grow five-fold to USD 4.2 billion by 2030, and then potentially to $30–35 billion by 2047.

Now, let’s look at some of the key services offered by modern CDMOs within a CDMO 2.0 model:

The CDMO 2.0 model lays more focus on integrated services so as to eliminate handoffs between different vendors; thereby offering a seamless progression from early-stage development through commercial manufacturing. Future-driven CDMOs today invest in innovative manufacturing equipment, process automation, AI-driven analytics, and digital quality systems (e.g., e-BMRs, LIMS) to enhance efficiency, quality control, and decision-making.

As regulatory support and quality control are critical parameters, CDMOs can provide extensive expertise in navigating complex global regulatory landscapes (e.g., FDA, EMA, ICH guidelines) and maintaining rigorous GMP standards. Scalability and flexible manufacturing are other important traits that CDMO brings to the table. The 2.0 model provides scalable infrastructure and flexible manufacturing platforms to meet demand across all clinical phases and commercial production, allowing small biotechs and large pharma alike to manage costs and capacity constraints.

Ultimately, the CDMO 2.0 model positions CDMOs as strategic innovation partners rather than mere service providers, offering comprehensive expertise and infrastructure to accelerate time-to-market for complex therapies.

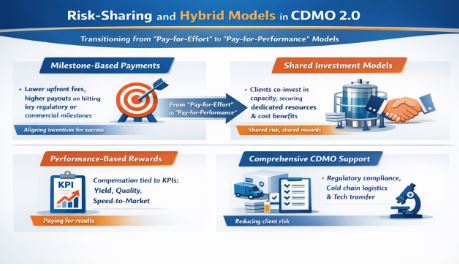

With the onset of risk-sharing, it marks a departure from traditional "pay-for-effort" contracts. It has moved to "pay-for-performance" models, wherein, CDMOs share in the success or failure of the drug.

Furthermore, in the CDMO realm, the milestone-based payments model has gained traction.

Here, CDMOs accept lower upfront fees in exchange for higher payments upon successful achievement of regulatory or commercial milestones; creating a win-win situation of both the stakeholders aligning the incentives of both partners.

Adding to this, companies now use ‘shared investment models’ rather than the CDMO bearing all capital expenditure. Companies now use "shared investment models," wherein, clients invest in capacity (e.g., bioreactors), and in return, secure dedicated capacity, lower pricing, or production credits.

Also, compensation is linked to KPIs such as yield, quality standards, or speed-to-market milestones. CDMOs now also take on responsibilities for regulatory compliance, cold chain logistics, and technology transfer, reducing the client's exposure to regulatory penalties or shipment losses. Hybrid Partnership Models

Hybrid models combine the best elements of traditional and modern outsourcing, balancing efficiency with specialized capability.

Integrated End-to-End Services: Many companies are moving away from multiple vendors for CRO (research) and CMO (manufacturing) services, opting for a single partner to manage the entire lifecycle. This reduces the risks associated with technical handoffs and technology transfers.

Boutique + Large CDMO Mix: Large companies often use "mega-CDMOs" for large-scale commercial production, while simultaneously partnering with boutique CDMOs for highly specialized capabilities like cell/gene therapies (CGT) or highly potent APIs.

Early-Stage Collaboration: CDMOs are increasingly involved in the process development stage, helping to design processes that are efficient to scale (e.g., using continuous flow technology)

Today, in the market packed with CDMOs, pharma companies must partner with a competent solutions provider. The leaders in this niche space have been spearheading the overall market’s growth by showcasing precision in driving innovation and setting benchmarks for others to follow.

As big pharma companies are looking for quality, digital tools, and talent, the CDMO 2.0 model is well-positioned to address some of the biggest hurdles pertaining to capacity bottlenecks due to high demand, talent acquisition in specialized areas like biologics, stringent regulatory audits requiring continuous compliance, customization demands; balancing client-specific needs with efficiency, significant investment in facilities, tech, and compliance, and Data & IP security to ensure protection of proprietary client data.

Lets delve into the key factors big pharma looks for in a CDMO partner from a 2026 perspective:

The shift toward novel therapies means generalist manufacturers are less attractive than specialists.

To speed up time-to-market, pharma companies prefer one-stop-shop partners to reduce coordination complexity.

The ability to handle rapid, unpredictable shifts in volume is critical in 2026.

The 2026 partnership model is built on trust and shared accountability.

According to part one of the Biobeat Report 2026, released by research and analytics firm De Facto ahead of CPHI Frankfurt, the world’s largest CDMO gathering, the global outsourcing market remains stable, regional growth will be uneven.

In the foreseeable future, China and the United States are positioned for stronger medium-term expansion, while India’s growth is expected to slow slightly in 2026 after a robust performance last year.

The analysis, prepared by Brian Scanlan, Executive Advisor at Edgewater Capital and Managing Partner at Freedom Bioscience Partners, draws on data from venture capital flows, licensing, IPO activity, and M&A trends to provide a global outlook for 2026.

While India remains a preferred outsourcing base for Western drugmakers, emerging tariffs and reshoring initiatives in the United States could alter outsourcing flows. 2026 has indeed been a reset year for India, depending on how trade policies evolve and how US–China relations influence the sector.

Despite these headwinds, Indian CDMOs are expected to retain their pricing advantage over Western competitors. With rising price pressures in the US and Europe due to regulatory reforms and drug pricing controls, India’s manufacturing base and technical depth continue to make it an attractive destination.

According to ICRA and CRISIL, India’s CDMO market is estimated at around USD 12–13 billion and has grown by double digits in recent years. Growth has been driven by rising global demand for complex generics, biologics, and specialised formulation development.

The Biobeat 2026 report projects mid-single-digit growth for the global CDMO sector this year, with India’s share led by investments in biologics, peptides, and sterile fill-finish capabilities. Expansion in aseptic manufacturing and high-potency compound handling, particularly in antibody-drug conjugates (ADCs) and bioconjugates, is expected to support Indian CDMOs that focus on specialised technologies rather than large-scale operations.

However, to spread your presence and attract business, three variables must converge:

1. A tangible development or manufacturing need

2. Available funding to support the work

3. Being at the right place at the right time

Even then, many CDMOs—especially small and mid?sized organizations—find themselves blocked by structural barriers. Large pharma and well?funded biotechs increasingly rely on preferred vendor lists as a cost?control mechanism. This trend has intensified as companies consolidate suppliers to gain pricing leverage.

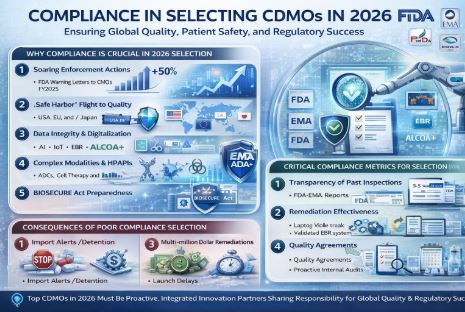

Robust regulatory compliance is the single most critical factor in selecting a Contract Development and Manufacturing Organization (CDMO) in 2026, shifting from a "checkbox" exercise to a strategic, proactive, and technology-driven requirement.

As pharmaceutical companies face increased scrutiny, supply chain complexities, and high-stakes innovations like biologics, selecting a partner with a flawless FDA, EMA, or equivalent record is essential to mitigate impending risks.

The 2026 landscape is characterized by "proactive regulatory readiness," where top CDMOs anticipate shifts in global guidelines and maintain continuous audit preparedness rather than simply preparing for inspections.

When evaluating a CDMO, 2026 best practices require auditing more than just a "clean" history:

In 2026, failure to properly vet a CDMO leads to:

Ultimately, the best 2026 CDMO partner is one that acts as an integrated innovation partner, sharing the responsibility for global quality, patient safety, and regulatory success.

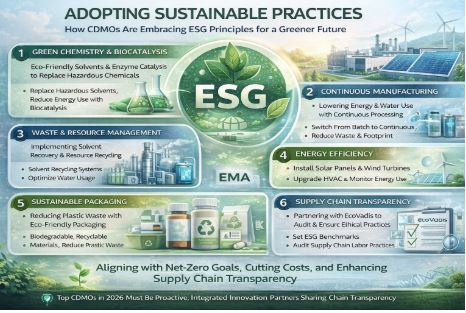

CDMOs are rapidly adopting ESG (Environmental, Social, and Governance) practices by shifting to green chemistry, implementing continuous manufacturing, and using renewable energy to reduce carbon footprints.

Key actions include adopting solvent recovery systems, utilizing single-use bioreactors to minimize water use, and adopting sustainable packaging.

1. Green Chemistry & Biocatalysis: The focus on replacing hazardous solvents with eco-friendly alternatives and using enzymes to reduce energy-intensive catalysis are on the rise today.

2. Continuous Manufacturing: We are also witnessing the much-needed switching from batch to continuous processes, thereby lowering energy consumption, reduces waste, and requires smaller facility footprints.

3. Waste & Resource Management: Implementing solvent recycling systems (distillation columns) to purify solvents like acetonitrile.

4. Energy Efficiency: Using smart meters, updating HVAC systems, and installing solar or other renewable energy sources, notes Laboratorios Rubió.

5. Sustainable Packaging: Using biodegradable materials and reducing plastic waste.

6. Supply Chain Transparency: Collaborating with organizations like EcoVadis to audit, set benchmarks, and ensure ethical labor practices.

7. ESG Reporting: Aligning with frameworks like CSRD or IFRS S1/S2 and setting science-based targets for net-zero emissions, says Neuland Labs.

CDMOs are focusing on these initiatives to meet regulatory demands, decrease operational costs, and satisfy client requirements for low-carbon supply chains.

he CDMO industry is experiencing a strong upward growth trajectory, with the global market projected to grow at a CAGR of roughly 7 percent to 8.7 percent through 2030–2032. India is poised to play a defining role not only domestically but at the global front; spearheading the niche with optimal precision. The Indian industry is transitioning from transactional, batch-by-batch relationships to long-term, integrated lifecycle partnerships, with a focus on specialized modalities like biologics and cell & gene therapy (CGT).

By 2030, the global CDMO market is expected to reach USD 230–280 billion, with top CDMO companies potentially commanding 40 percent of the market due to mergers and acquisitions. The future will favor "mega-CDMOs" offering end-to-end services, as well as specialized, "boutique" CDMOs that can offer specialized expertise, agility, and high-tech capabilities in specialized areas.

.jpg)

.jpg)

Through Collaborative Efforts")

, CDSCO.jpg "Fostering a Quality Culture in the Pharmaceutical Industry")