Zeenat Parween, Correspondent, India Pharma Outlook

")

Indian pharma stocks have been one of the more interesting corners of the stock market lately.

While several other sectors wobbled through bouts of volatility in early 2026, pharmaceutical companies largely held their ground — and in some cases, rallied hard.

That's not an accident. It reflects a mix of steady domestic medicine demand, a wave of new product launches, and the fact that healthcare spending doesn't really pause just because the broader economy gets choppy.

This is exactly why Indian pharma stocks are getting fresh attention from investors right now. The sector's defensive character combined with genuine earnings momentum at several large companies, has pulled money back into pharma counters.

Brokerages have also flagged the sector as one of their preferred picks for 2026, citing improving domestic growth and a slow but real shift toward higher-margin specialty products.

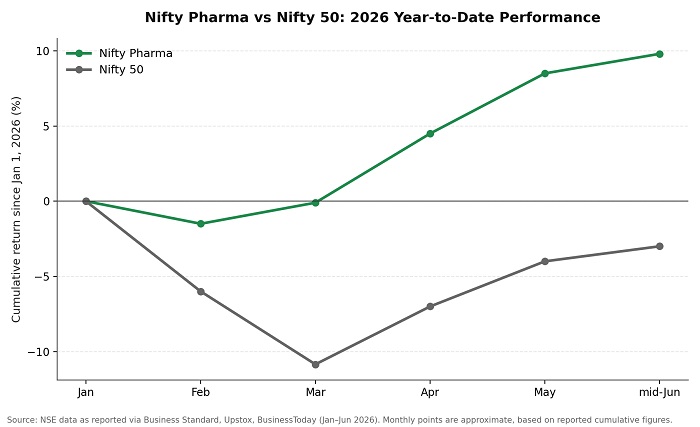

Zooming out, the Nifty Pharma index has had a strong run. NSE data shows the index gained close to 9.8 percent on a year-to-date basis by May 2026, even as the broader Nifty 50 struggled with foreign investor outflows and geopolitical noise.

In fact, from January 1 to March 25, 2026, Nifty Pharma was nearly flat at -0.10 percent, while the Nifty 50 fell almost 11 percent — a striking gap that shows just how much the sector cushioned investor portfolios during a difficult stretch for the broader market. By mid-June, the index was trading around the 24,000–24,400 range, having touched a 52-week high of 25,043.15 earlier in the quarter.

None of this means every pharma stock did well. Some of the biggest, most recognizable names — including a couple of companies most investors would assume are "safe" pharma bets — actually posted sharp profit declines in the latest quarter because of a single drug patent expiry in the US. So this isn't a simple "buy the whole sector" story. It's a story about which companies adapted, which got hurt, and which are quietly building the next leg of growth.

In this article, we examine the best-performing Indian pharma stocks of the January–March 2026 quarter and the factors that drove their performance. Using a combination of stock market returns, quarterly earnings, business fundamentals, and management commentary, we identify the companies that stood out during the period. We also compare their results, assess key industry trends, highlight risks and opportunities, and explore what the rest of 2026 could hold for the Indian pharmaceutical sector.

Also Read: Scaling Perfusion Technology from Lab Success to Manufacturing Reality

The clearest sign of pharma's relative strength this quarter came from the Healthcare Index, which outperformed the Sensex by roughly 12 percentage points during the January–March 2026 period. That's a meaningful gap, and it happened during a stretch when foreign institutional investors were net sellers across much of the market. Investors moved into pharma precisely because it's seen as a defensive sector.

Three things stand out. First, India's domestic pharmaceutical market itself grew strongly — Pharmarack data shows the Indian pharma market grew 10.3 percent in April 2026, led by anti-diabetes, cardiac, and respiratory therapies. Second, several companies pushed harder into specialty medicines, biosimilars, and innovative drugs rather than relying purely on commodity generics — a shift management teams across Sun Pharma, Dr. Reddy's, Cipla, and Lupin have openly discussed on recent earnings calls. Third, a wave of new product launches, including generic Semaglutide hitting the market in March 2026, gave a fresh tailwind heading into FY27.

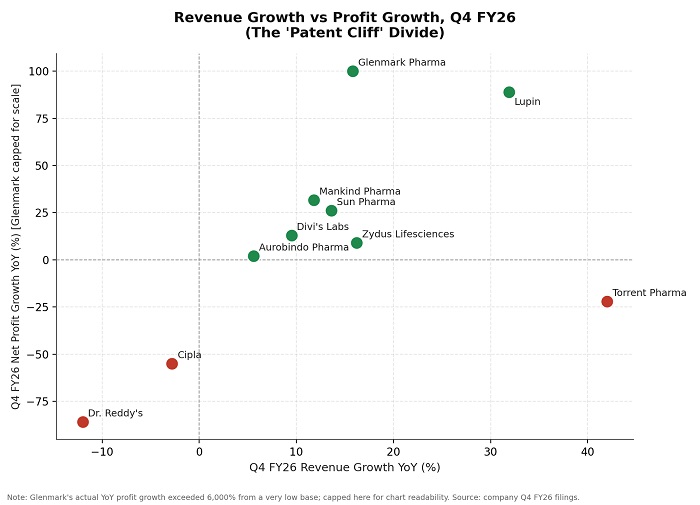

Here's where it gets nuanced. Domestic formulations were the clear bright spot — organic India sales grew in the low-to-mid double digits for most large companies, driven by chronic therapy demand and steady acute treatment volumes. Export markets told a more mixed story. The US business, in particular, was hit hard for some companies because of the gRevlimid patent cliff — the generic version of a major blood cancer drug lost its exclusivity protection in January 2026, and analysts at ICICI Securities had flagged this would disproportionately hurt Dr. Reddy's, Zydus Lifesciences, and Cipla. That single event explains a lot of the profit volatility you'll see in the company breakdowns below.

USFDA approvals continued at a healthy paceacross the sector — Aurobindo Pharma alone received final approval for 9 ANDAs (Abbreviated New Drug Applications) in the quarter and had filed 888 cumulative ANDAs by the end of FY26. Meanwhile, M&A activity reshaped the competitive landscape: Torrent Pharmaceuticals completed its acquisition of a controlling stake in JB Chemicals & Pharmaceuticals in January 2026, and Glenmark signed a landmark licensing deal with AbbVie worth up to USD 1.925 billion for an oncology and autoimmune disease asset built on its BEAT protein platform.

Metric | Q4 FY26 | Trend |

Nifty Pharma YTD return (as of May 2026) | +9.8 percent | Outperforming Nifty 50 |

Healthcare Index vs Sensex (Jan–Mar 2026) | +12 pts relative outperformance | Strong |

Indian pharma market growth (April 2026) | +10.3 percent | Domestic demand-led |

Sector-wide revenue growth estimate (Q4 FY26) | ~7.2 percent | Per ICICI Securities |

Sector-wide net profit estimate (Q4 FY26) | -13.3 percent | Hit by gRevlimid patent cliff |

1. Sun Pharmaceutical Industries

1. Sun Pharmaceutical IndustriesSun Pharma remains India's largest pharmaceutical company, and its Q4 FY26 results back that position up. Consolidated net profit rose 26.2 percent year-on-year to Rs 2,714 crore, on revenue of Rs 14,612 crore, up about 13 percent YoY. For the full year, sales touched Rs 58,220 crore.

Key Business Segments: The standout this quarter was the Global Innovative Medicines business, which crossed USD 1.4 billion in FY26 sales and now makes up more than 22 percent of consolidated revenue. India formulations also grew a strong 14.8 percent in the quarter, with the company's domestic market share rising from 8.1 percent to 8.4 percent, per Pharmarack data.

Recent Developments: The company launched 37 new products during FY26 and declared a Rs 5 per share dividend. Its US generics business was roughly flat, with growth in innovative medicines offsetting that softness.

Growth Outlook: Management has pointed to specialty drugs like Ilumya gaining traction in newer markets such as Romania and Brazil as a long-term growth lever beyond the traditional generics business.

Sun Pharma remains India's largest pharmaceutical company and a leading player across specialty medicines and generics. As Aalok Shanghvi, the company's Chief Operating Officer, put it on the Q4 FY26 earnings call, innovative medicines have become an important new growth driver in emerging markets.

Dr. Reddy's full-year FY26 revenue grew 3.2 percent to Rs 33,593 crore, but Q4 FY26 alone saw profit after tax crash 86 percent year-on-year to around Rs 220 crore. The reason: a sharp 51 percent YoY collapse in North America revenue, driven heavily by the gRevlimid patent expiry, plus a Rs 453 crore stock adjustment and pricing erosion in key markets.

Global Expansion Strategy: Europe revenue jumped 55 percent for the full year, and Emerging Markets grew 23 percent. India business grew a healthy 16 percent to Rs 6,219 crore for the year, showing the domestic franchise remains solid even as the US business resets.

Investor Takeaways: The sharp Q4 profit drop is largely a one-off patent-cliff effect rather than a structural problem, but investors will want to see North America stabilise before getting too confident about FY27. The company still recommended a final dividend of Rs 8 per share, signalling management's confidence in the underlying cash flow despite the rough quarter.

Cipla's Q4 FY26 numbers also took a hit from the patent cliff — consolidated net profit fell 55 percent YoY to Rs 554.6 crore, with revenue down about 3 percent to Rs 6,541 crore. North America revenue dropped 26 percent due to product losses. But the India business was a genuine bright spot, growing 15 percent YoY, helped by in-licensing partnerships, including bringing in Eli Lilly's obesity drug and certain Pfizer products into its portfolio.

Respiratory Segment Leadership: Cipla continues to strengthen its respiratory portfolio and has outlined major product launches supporting future growth, a segment where it has historically held a leading domestic position.

Future Product Pipeline: Management has guided for EBITDA margins of 18.5–20 percent for the coming year and is targeting a USD 250 million US revenue run-rate by Q4 FY27, suggesting they expect the North America business to recover from this quarter's lows. Notably, the stock actually rose over 8 percent on the day results were announced, suggesting the market had already priced in much of the bad news.

Torrent has long been known for its strength in chronic disease therapies within India, and that domestic strength showed up again this quarter, with base-business growth (excluding the JB Pharma acquisition) running at 16 percent.

International Expansion: Revenue jumped 42 percent YoY to Rs 4,197 crore in Q4 FY26, largely because of the newly completed JB Chemicals & Pharmaceuticals acquisition, finalised on January 21, 2026. US and Brazil businesses grew 24 percent each for the full year, while Germany grew 10 percent despite supply chain challenges.

Growth Drivers: Net profit actually fell about 22–27 percent YoY to roughly Rs 364–389 crore (reports vary slightly depending on whether exceptional items are included), due to higher integration-related expenses. The company is also seeking shareholder approval for a Rs 5,000 crore fundraise (QIP) to support further expansion, and expects the JB Pharma merger to deliver Rs 450 crore in cost synergies by FY29.

Divi's is India's largest manufacturer of Active Pharmaceutical Ingredients (APIs), and it delivered one of the cleaner, less dramatic quarters on this list. Consolidated profit after tax rose 13 percent YoY to Rs 751 crore, with revenue up nearly 10 percent to Rs 2,831 crore.

Export Opportunities: Divi's business model is heavily export and custom-synthesis driven, supplying APIs to global pharma majors. A strong forex gain during the quarter added to profitability.

Competitive Advantages: The company maintains very low debt levels relative to peers and announced a generous final dividend of Rs 30 per share, a 1500 percent payout on face value, reflecting confidence in its cash position. EBITDA margins did dip slightly to 33 percent from 34.3 percent a year earlier, linked to changes in business mix, but profitability remains among the strongest in the sector.

6. Zydus Lifesciences

Zydus reported consolidated net profit of Rs 1,273 crore in Q4 FY26, up roughly 9 percent YoY, with revenue rising over 16 percent to Rs 7,587 crore. That's a notably better outcome than peers like Dr. Reddy's and Cipla, even though Zydus was also flagged as exposed to the gRevlimid patent cliff heading into the quarter — suggesting the company managed the transition better than expected.

Market Expansion Strategy: The stock surged more than 7 percent on results day, pushing the Nifty Pharma index to a fresh 52-week high. Zydus also announced a share buyback worth up to Rs 1,100 crore, a signal of management's confidence in the stock's valuation. Bernstein has rated Zydus as one of its preferred picks in the sector, citing its specialty medicines push and expanding global market presence.

Mankind Pharma is almost entirely a domestic-focused story, and that worked in its favour this quarter. Net profit jumped 31.75 percent YoY to Rs 554.35 crore in Q4 FY26, with sales rising 11.81 percent to Rs 3,442.93 crore.

Chronic Disease Portfolio Expansion: The company engages with over 5 lakh doctors across India and continues to expand its presence in chronic therapies, an area benefiting from growing diagnosis rates and treatment adherence nationally.

Earnings Momentum: Mankind Pharma has benefited from growing demand in chronic therapies and improved market share. That said, full-year FY26 net profit actually declined 3.92 percent to Rs 1,912.93 crore, even as full-year sales rose nearly 17 percent — a reminder that one strong quarter doesn't erase a softer year overall. The stock has nonetheless been a favourite among momentum-focused investors through 2026.

Lupin delivered one of the more dramatic turnarounds on this list. Consolidated net profit for Q4 FY26 came in at roughly Rs 1,460–1,468 crore, up about 89 percent year-on-year, on net sales of Rs 7,474.66 crore, a 31.89 percent YoY jump.

Global Market Presence: US sales rose 46 percent to Rs 11,678 crore for the year, contributing 42 percent of global sales, while the company also expanded its European footprint through acquisitions including Renascience Pharma in the UK and VISUfarma in the Netherlands. Managing Director Nilesh Gupta said the results reflect strength and resilience across key geographies, with both the US and India delivering strong sales growth.

Investor takeaway: Lupin's stock has delivered over 18 percent returns in the past year and more than 224 percent over three years, comfortably outperforming broader indices, while trading at a notably cheaper valuation (around 22.6x earnings) than several premium peers.

Aurobindo posted record quarterly revenue of Rs 8,853 crore in Q4 FY26, up 5.6 percent YoY, with the US formulations business contributing USD 387 million, around 40 percent of consolidated revenue.

Manufacturing Strength: As one of the world's top five producers of semi-synthetic penicillins, Aurobindo continues to lean on scale manufacturing. The company also completed the acquisition of Khandelwal Laboratories' non-oncology business for USD 317 million during the year.

Net profit, however, was nearly flat — up only about 2 percent YoY to Rs 921 crore — as elevated employee costs and operating expenses ate into the benefit of higher sales. Management has guided for EBITDA margins above 21 percent in FY27, an improvement from the 20.3 percent reported in Q4 FY26, and the company's biosimilars arm, CuraTeQ Biologics, continues to expand its pipeline toward a total addressable market estimated at USD 50 billion over the next decade.

Glenmark had one of the standout turnaround stories of the quarter. Consolidated net profit jumped to Rs 301.41 crore in Q4 FY26, up sharply from just Rs 4.65 crore in the same quarter last year (a low base, but still a meaningful operational recovery). Revenue rose nearly 16 percent YoY to Rs 3,760–3,771 crore.

Emerging Opportunities in Metabolic Health: Glenmark has strengthened its presence in newer therapeutic segments including metabolic health, alongside continued momentum in respiratory and oncology. The company launched GLIPIQ for diabetes and expanded its respiratory portfolio with Nebzmart GFB Smartules during the year.

Future Growth Potential: The biggest headline of the year was a licensing deal with AbbVie for ISB 2001, an oncology and autoimmune disease asset, worth up to USD 1.925 billion including a USD 700 million upfront payment. Chairman and Managing Director Glenn Saldanha called FY26 a defining year in the company's evolution, pointing to the launches of generic respiratory products in the US that demonstrate continued therapeutic expertise. Full-year FY26 PAT rose 30.1 percent to Rs 1,362 crore on revenue growth of 27.5 percent.

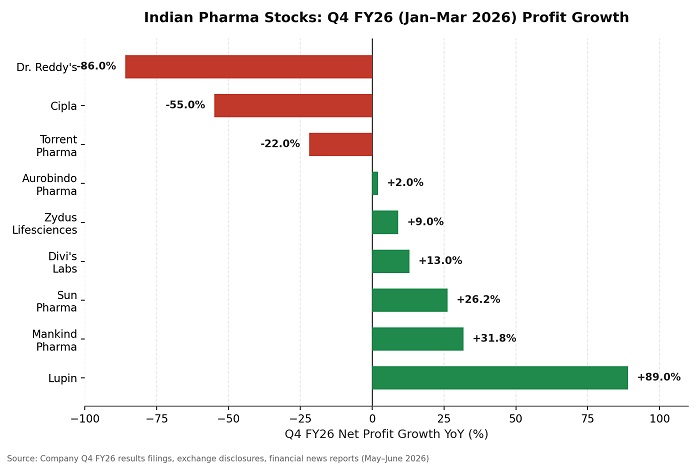

Putting these companies side by side makes the patterns easier to see. A few things jump out immediately: the gRevlimid patent cliff clearly separated the sector into two camps this quarter — companies heavily exposed to that single US generic drug (Dr. Reddy's, Cipla, and to a lesser extent Zydus) saw sharp profit hits, while companies with more diversified, India-heavy, or specialty-driven portfolios (Sun Pharma, Lupin, Mankind, Glenmark) posted strong profit growth.

Company | Q4 FY26 Revenue | Q4 FY26 Net Profit | YoY Profit Growth | Outlook |

Sun Pharma | Rs 14,612 cr | Rs 2,714 cr | +26.2 percent | Strong, specialty-led |

Dr. Reddy's | Rs 7,516 cr | Rs 220 cr | -86 percent | Recovery-dependent on US |

Cipla | Rs 6,541 cr | Rs 555 cr | -55 percent | India strong, US rebuilding |

Torrent Pharma | Rs 4,197 cr | Rs 364-389 cr | -22 percent to -27 percent | Integration-led, base business solid |

Divi's Laboratories | Rs 2,831 cr | Rs 751 cr | +13 percent | Steady, export-driven |

Zydus Lifesciences | Rs 7,587 cr | Rs 1,273 cr | +9 percent | Resilient, buyback announced |

Mankind Pharma | Rs 3,443 cr | Rs 554 cr | +31.75 percent | Strong domestic momentum |

Lupin | Rs 7,475 cr | ~Rs 1,460 cr | +89 percent | Best turnaround story |

Aurobindo Pharma | Rs 8,853 cr | Rs 921 cr | +2 percent | Margin pressure, record sales |

Glenmark Pharma | Rs 3,760 cr | Rs 301 cr | Sharp recovery from low base | AbbVie deal a major catalyst |

Rising global demand for generic medicines continues to be the backbone of export revenue for most Indian pharma majors, even as pricing pressure persists in mature markets like the US.

Rising global demand for generic medicines continues to be the backbone of export revenue for most Indian pharma majors, even as pricing pressure persists in mature markets like the US.

Growth in specialty and complex generics is where the real margin expansion is happening. Sun Pharma's Global Innovative Medicines business and Aurobindo's biosimilars pipeline are good examples of companies betting on higher-value, harder-to-replicate products rather than commodity generics.

Increased healthcare spending within India — driven by rising incomes, insurance penetration, and chronic disease prevalence — is the single biggest reason domestic formulations businesses have outgrown export businesses across nearly every company on this list.

API manufacturing expansion remains a structural tailwind, with companies like Divi's and Aurobindo's CuraTeQ unit scaling capacity to capture both API export demand and CDMO (contract development and manufacturing) opportunities.

Opportunities from global supply chain Diversification — as global pharma companies look to reduce dependence on any single sourcing geography, India's manufacturing base stands to benefit, though this remains more of a medium-term thesis than a quarter-by-quarter driver.

Growing Chronic Disease Market in India — particularly diabetes, cardiac conditions, and respiratory illness — is consistently cited by Mankind Pharma, Torrent, and Sun Pharma as their most reliable growth engine.

Performance of Large-Cap Pharma Stocks

Performance of Large-Cap Pharma StocksThe large-caps in this list — Sun Pharma, Dr. Reddy's, Cipla — delivered a genuinely mixed bag. Sun Pharma was the standout, while Dr. Reddy's and Cipla both took real hits from the patent cliff. This shows that size alone doesn't protect against company-specific risk events.

Mid-sized names had some of the most exciting stories this quarter. Lupin's 89 percent profit jump and Glenmark's dramatic turnaround (helped by the AbbVie deal) both came from companies in the mid-cap to large-mid-cap range, while Mankind Pharma's pure-domestic model kept delivering consistent growth without exposure to US patent risk.

Broadly, large-caps offer more stability and dividend consistency but were this quarter's biggest victims of single-event risk (the patent cliff). Mid-caps offered higher growth and turnaround potential but can be more volatile and dependent on company-specific catalysts like licensing deals or new launches.

Conservative, income-focused investors have typically leaned toward names like Divi's and Sun Pharma for their stronger balance sheets and dividend history. Growth-focused investors have been more drawn to Lupin, Glenmark, and Mankind Pharma, given their sharper earnings momentum this quarter.

This is where balance matters most — the pharma rally has real substance, but it isn't risk-free.

Regulatory Risks: Pricing controls, drug recalls, and changes to import/export rules in key markets can all move stock prices quickly and unpredictably.

USFDA Compliance Factors: Every Indian pharma exporter to the US depends on maintaining clean USFDA inspection records at its manufacturing plants. A single warning letter or import alert at a key facility can dent revenue for several quarters.

Export Dependency: This quarter showed exactly why over-dependence on a handful of US products is risky — the gRevlimid patent cliff alone wiped out a meaningful chunk of profit at multiple companies. Diversified revenue across India, the US, Europe, and emerging markets tends to smooth out this kind of shock.

Research and Development Spending: Companies investing meaningfully in R&D — Sun Pharma spent Rs 975.7 crore (6.7 percent of sales) in Q4 FY26 alone — are generally better positioned for the next wave of specialty and biosimilar growth, though heavy R&D spend can also pressure near-term margins.

Product Pipeline Strength: Look at ANDA approvals, biosimilar progress, and licensing deals (like Glenmark's AbbVie partnership) as indicators of future, not just current, growth.

Valuation Considerations: With some stocks trading above 60-70x earnings and others below 25x, valuation discipline matters. A great company bought at too high a price can still be a poor investment.

Brokerages have been broadly constructive but selective. Multiple analysts including those at Kotak, PL Capital, and JM Financial flagged Sun Pharma, Torrent Pharma, Lupin, and Anthem Biosciences as preferred picks heading into the quarter, while flagging Cipla, Zydus, and Dr. Reddy's for likely weakness tied to the patent cliff — a forecast that largely played out as expected.

Analysts broadly expect earnings growth to gradually improve as the impact of the gRevlimid patent cliff fades from year-on-year comparisons later in FY27, combined with continued strength in domestic formulations and the ramp-up of newer launches like generic Semaglutide.

The sector isn't universally cheap — premium names like Divi's and Torrent trade at rich multiples — but there's still a meaningful spread, with names like Lupin and Dr. Reddy's trading at more reasonable valuations relative to their growth potential, assuming the US business stabilises.

The sector continues to benefit from defensive characteristics, strong domestic demand and export opportunities. The main risks ahead are further US pricing pressure, regulatory surprises, and the pace at which companies can successfully pivot from commodity generics to higher-value specialty products.

A pure-play API and formulations manufacturer that has continued to expand its finished-dosage business, often discussed as a smaller, more focused alternative to the larger generics players.

India's leading biosimilars company, Biocon continues to be closely watched for its global biosimilar approvals and partnerships, even though Bernstein rated it "Underperform" in its recent coverage initiation, citing near-term execution concerns.

A domestically focused company with strong positioning in anti-infectives and a brand portfolio that brokerages like ICICI Securities have flagged as a top pick for India-focused growth.

A CDMO (contract development and manufacturing) and complex hospital generics player, Piramal Pharma has been flagged by some brokerages for a relatively subdued quarter, reflecting the broader CDMO segment's softer near-term demand environment.

Beyond the well-known names, companies like Caplin Point, JB Chemicals (now part of Torrent), Concord Biotech, and Ajanta Pharma have been cited in market data for strong margin profiles and low leverage, making them worth a closer look for investors willing to dig past the headline large-caps.

With the immediate drag from the gRevlimid patent cliff expected to ease as FY27 progresses, and domestic demand growth running consistently above 10 percent, most brokerages expect earnings growth to re-accelerate through the back half of 2026 and into 2027.

Global supply chain diversification, continued USFDA approvals, and the gradual shift toward complex generics and biosimilars all point to export revenue staying an important growth pillar, even if it's a bumpier ride than the domestic business.

The clearest structural story in this entire article is the sector-wide pivot toward specialty medicines, biosimilars, and innovative drugs — visible in Sun Pharma's Global Innovative Medicines business, Glenmark's AbbVie licensing deal, and Aurobindo's CuraTeQ biosimilars platform.

While not the dominant theme of this quarter's results, several companies have begun referencing digital health tools and AI-assisted drug discovery in investor presentations, an area likely to get more airtime in future earnings calls as the technology matures.

India's pharmaceutical market is expected to continue expanding, supported by domestic healthcare demand and global exports. The companies best positioned for the next phase appear to be those balancing a stable India franchise with a genuine, well-funded push into specialty and biosimilar products — rather than those relying purely on commodity generics.

Based on Q4 FY26 (January–March 2026) earnings growth, Lupin delivered the strongest turnaround with an 89 percent jump in net profit, while Mankind Pharma (31.75 percent profit growth) and Sun Pharma (26.2 percent profit growth) also stood out. On pure stock momentum, Zydus Lifesciences and Mankind Pharma drove the Nifty Pharma index to fresh 52-week highs during the quarter.

Sun Pharma, Dr. Reddy's, Cipla, Lupin, and Aurobindo Pharma all have substantial US and international operations, with Sun Pharma's Global Innovative Medicines business and Aurobindo's US formulations business (around 40 percent of its consolidated revenue) standing out as particularly significant global franchises.

This isn't investment advice, but based on the data here, investors often look at companies with strong balance sheets, diversified revenue, and consistent dividend history — Sun Pharma, Divi's Laboratories, and Lupin are frequently mentioned by brokerages in this context, given their combination of scale, low debt, and visible growth pipelines. As always, individual suitability depends on your own goals, risk tolerance, and time horizon — it's worth speaking with a registered financial advisor before making investment decisions.

Indian pharmaceutical companies are increasingly positioned as global healthcare leaders. Investors should focus not only on quarterly stock performance but also on earnings quality, product pipelines, regulatory compliance, and long-term growth prospects. This quarter was a useful reminder that even strong, well-run companies can take a hit from a single event like a patent expiry — which is exactly why looking at the full picture, rather than one number, matters so much in this sector.

We built this piece around one constraint: every number had to be real and traceable, not estimated or smoothed over for narrative convenience. That meant working with the most recently completed quarter (Q4 FY26) rather than the current one, since April–June 2026 results simply aren't out yet. A few names on this list had rough quarters on paper but we've kept those numbers in rather than cherry-picking only the good news. If you're using this article to inform investment decisions, treat it as a starting point for your own research, not a final word.

Through Collaborative Efforts")

, CDSCO.jpg "Fostering a Quality Culture in the Pharmaceutical Industry")